Pre Month End

This document assumes that the accountant (or person responsible) is ultimately responsible for producing accurate month end values in a variety of modules. It may of course be that multiple people each carry out elements of these tasks however this document is compiled as though it is one person.

There are a number of considerations to be made at the calendar month's end. These include values which either would be very difficult to achieve (e.g. a Parts Valuation could be achieved after month end by using the Movements Report) or cannot be reversed back to the Month End values (such as End of Day/ Month reports).

At Calendar Month End

Parts Valuation

In order to provide the correct position for stock at the month end it is necessary at close on the last day to complete a Parts Valuation Report. The information required is the Valuation by Product Group and also the Aged Values. These reports in addition to the Work In Progress and the GINR report will later be used to provide Parts Stock reconciliation to the Nominal Ledger. This report is best downloaded to allow for reconciliation later.

Parts Aged Valuation

Dependent on the policy of the site if obsolescence provisions are taken then this report at calendar month will be required to provide the provisioned value

Work In Progress Report

Again this is required to complete the Parts Stock reconciliation and also to act as supporting documentation for confirming Technician Statistics. This should be run at close on the last day.

GINR Report

The GINR report is the final document required for the reconciliation of Parts Stock as at close on the last day.

GRNI Report

In order to provide the necessary data should the GRNI nominal value fail to balance at month end the GRNI report in Purchase Ledger should be exported to Excel. This should also apply to the Purchase Ordering GRNI report.

Movement Report

In order to reconcile the Parts Deposit process it is necessary to run at the calendar month end a Movement Report between the dates required using the issue type of Deposit Invoices. This report provides details of all deposits taken within the period.

Parts in Transit (Internal Orders)

Where the distribution process is being used in Parts it is necessary to ensure that at Month End all parts sent out to other sites have been receipted. To ensure this the Parts in Transit Report should be run on the last day of the month.

Close down Exception Report

In order that nominal values are recorded in the correct period it is best practice to run the Close down Exception Report at the close of play on the last day of the month and complete all workshop invoices contained within it. Failure to do this will create difficulties in certain circumstances with the reconciliation of vehicles but will also result in the internal workshop sales being incorrect for the period.

Deposits Day Book

Should be run off the last day and ensure all outstanding cash postings are made. Reconciliation of this should take place on a daily basis and therefore at month end, there should be no need for further work.

Parts and Service EOD/EOM

Parts and Service should as a matter of course complete their day ends. Whilst they may wish to print only the pages required for their internal reporting, at Month End both the Day and Month End prints should be completed in their entirety. This is extremely important since certain information is only available at month end. This information may well be required by other areas of the business specifically accounts.

Once the above have been completed they should be retained in a file ready for the completion of the month end process. The month end needs to be completed to ensure that management accounts and manufacturer composites can be completed on time

All of the above reports as well as providing reconciling opportunities when the system month end close is being carried should be considered as part of the month end audit trail and as such should be filed in the month end audit pack.

System Close Month End Process

It is necessary at the end of each month to reconcile a number of reports within each module back to their nominal values. It may then be necessary subject to company requirements to complete a set of print outs as supporting documentation for the month end pack.

This process may be completed in any order however the most usual is Sales Ledger, Vehicles, Purchase Ledger and finally Nominal (there is no month end process within Cashbook).

Sales Ledger

Frequently Sales Ledger can be closed within a short time after month end. The main requirement before closing is that all cash postings should have been completed first.

Statements can be produced once cash has been posted, Statements run from the earlier period will include transactions paid during the period, and statements run from the later period will not.

Once all transactions are complete it is necessary to reconcile the Sales ledger nominal value back to the Sales Ledger Balance.

The ledger balance value should be taken by the Accounting Group and reconciled to the equivalent nominal value.

In the event of there being a discrepancy in the reconciliation, the outstanding transaction report should be printed and reviewed against the specific nominal code. Alternatively, it is possible to download the aged debt report into Excel and using a “vlookup” table, compare the download to the exported nominal value. Differences may occur where journal entries have taken place or timing differences created.

Once the Sales ledger values have been reconciled the Aged Debt and Transaction reports should be printed and added to the Month End Pack.

At this point, the Sales Ledger can be closed.

Vehicle Management

Vehicle Management should only be closed after all vehicle processes have been completed.

Before any month end processes are carried out the person responsible for Sales Performance should fully review the Profit by Deal report. It is essential that once this report is agreed no further changes should take place to the PBD affecting the profit. In many cases, the PBD is signed off by the Sales Department Leader and passed to the Accounts team to form part of the Month End Accounting pack (along with a signed off Closedown Exception Report)

Once all banking postings have been made reconciliations can be carried out.

These reconciliations can be performed in any order however it is probably advisable to leave stock reconciliation till last since it encompasses a number of nominal codes whereas the other reconciliations are too individual codes

Deposits require 2 reconciliations, reconciling un-banked values from the daybook to the Deposit Cash code, and customer deposits held to the Deposits nominal code.

As previously mentioned it is good practice to reconcile the daybook entries daily, if this has not been done then it should be completed at month end. The nominal value for the period should be exported and using the reference of the customer name reconciled to find any outstanding values. Outstanding values should then be reconciled to any unbanked payments. If a discrepancy still occurs this usually occurs due to posting being incorrectly made to the vehicle debtor rather than the deposit nominal. Alternatively, deposits may be posted to the customer after the vehicle has been invoiced in this case it is possible to clear the deposit to the debtor.

The Deposits Held reconciliation can then be carried out. The deposits report from vehicles should be produced from the date of the earliest held deposit and reconciled back to the nominal value for Deposits Held. The primary reference is the customer name although it may also be possible in many cases to use the stock number. In the event of discrepancy, a review of the vehicle stock card for those with discrepancies should reveal the cause of the problem.

The vehicle debtors should be the next report to reconcile. A full report of debtors should be completed between the debtors' report and the nominal value. It is important to ensure the debtors' report is taken for the correct period. In the event of discrepancies a download of the nominal code should be taken, a download of the debtor report and a “vlookup” table can be prepared to highlight any differences. Differences generally occur due to deposit postings being incorrectly made. In this case either clearing deposit postings using the CRM assign vehicle process or using a contra should clear any problems.

Vehicle Creditors

Before completing the Vehicle Creditor reconciliation it is important to ensure that there are no vehicles incorrectly held at a status of Unconfirmed. Any vehicle listed as unconfirmed has no nominal values posted therefore it is important to clear vehicles with this status first.

Vehicle creditors are held as consigned or adopted, in the case of consigned vehicles since on adoption the correct value will be confirmed consignment creditors simply need to provide an equal and opposite value to the consigned stock. Obviously, the consigned creditor must reconcile to the nominal code for consigned creditors.

Adopted vehicle creditors should be reconciled directly to the nominal value for adopted creditors, whilst completing the reconciliation the creditor type should be reviewed. In the event of a creditor value being incorrectly linked to the wrong type e.g. creditor value linked to the supplier when it should have been posted to RFL, a contra debiting Vehicle Management Payments and crediting Vehicle Management Payments allows the type to be corrected.

In the event of a difference between the vehicle creditor report and the nominal, both reports can be exported and reconciled using Excel.

Vehicle Stocks

In order to reconcile vehicle stocks the End of Period stock list should be used.

This must be run before month end is processed.

Although not essential it may be prudent to carry out a physical stock check at the end of each month, the stock should then agree back to the End of Period report.

The EOP stock list provides a breakdown by nominal ledger code of the stock values; it also shows any discrepancies between vehicle value and nominal value.

It should be remembered however that discrepancies are only shown for vehicles in stock, if a nominal value is held for a vehicle not in stock this will not appear on the EOP stock list. For this reason, it is necessary to ensure that the nominal value of the stock agrees with the vehicle value. In the event of discrepancies the end of period stock list can be filtered by nominal code this allows for the reconciliation of individual codes.

Overall if a difference is apparent in the stock value a download from the normal stock report can be completed and this is reconciled from the SIV to the outstanding nominal value.

Because the End of Period stockist cannot be downloaded due to its complexity of operation and where discrepancies frequently occur because of the site practices such as not clearing workshop jobs or making sales after the period end then it may be prudent to download a stock list including purchase price at calendar month end to provide at least a snapshot of the position at that time. Whilst this cannot be utilised for reconciliation purposes it may provide valuable information when the reconciliation takes place.

Once this has been completed reports should be printed for the End of Period audit pack. As a minimum, the EOP stock list, VAT analysis, debtors, creditors and deposit reports should be produced.

At this point Vehicles may be closed.

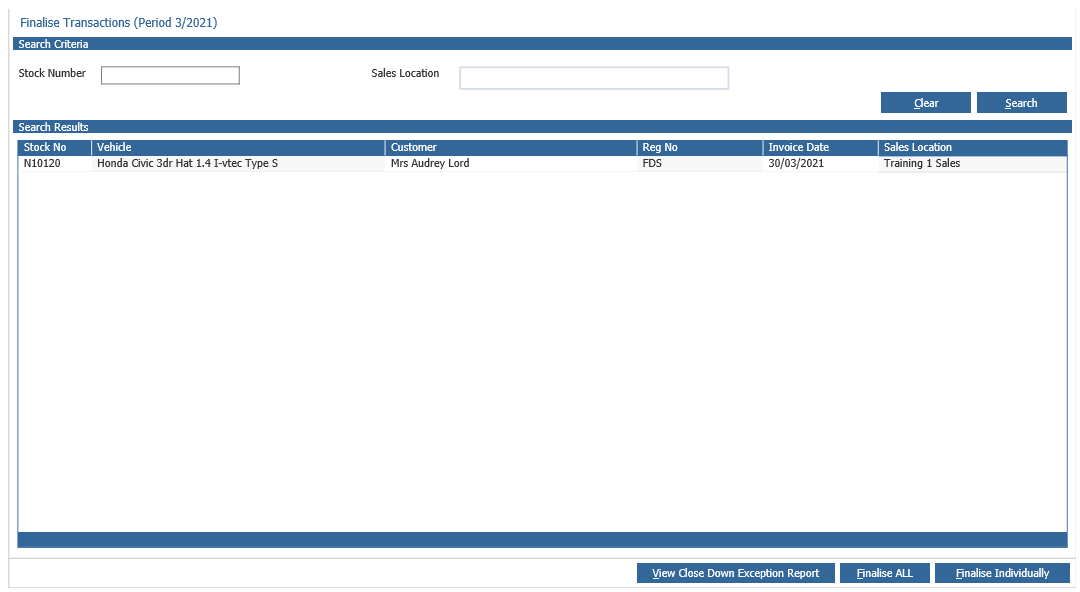

Finalise all deals first by clicking on the Finalise All option.

If any deals cannot be finalised, viewing the Closedown Exception Report will advise the reasons why and these will need to be processed before the deals can be finalised.

Purchase Ledger

Purchase Ledger is generally kept open to allow for the posting of invoices from the prior period. This depends on decisions made by the site although in a growing number of businesses, this only happens for a few days.

Automatic payments can be carried out during either open period.

Once all transactions are complete it is necessary to reconcile the purchase ledger nominal value back to the Purchase Ledger Balance.

The ledger balance value should be taken by the Accounting Group and reconciled to the equivalent nominal value.

In the event of there being a discrepancy in the reconciliation, the outstanding transaction report should be printed and reviewed against the specific nominal code. Alternatively, it is possible to download the aged credit report into Excel and using a “vlookup” table compare the download to the exported nominal value. Differences may occur where journal entries have taken place or timing differences created.

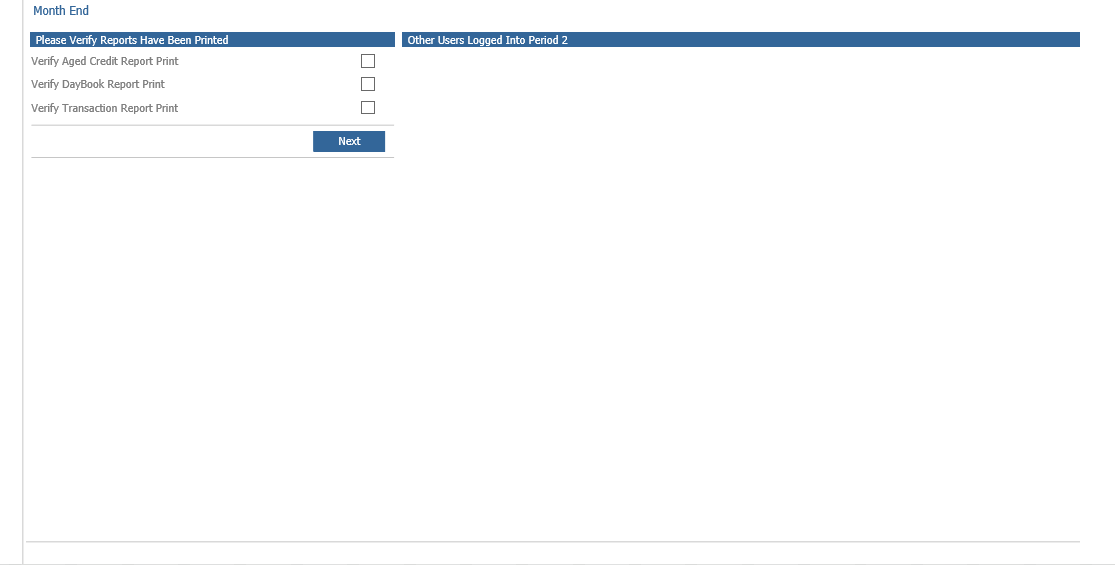

Once the purchase ledger values have been reconciled the Aged Credit and Transaction reports should be printed and added to the Month End Pack

At this point the Purchase Ledger can be closed.

Other Reconciliations

Other Reconciliations

Before completing the necessary work to close the Nominal Ledger a number of other reconciliations should take place.

Bank Reconciliation

There is no month end process required for Cashbook however in order to close the nominal a full Bank reconciliation should take place.

In many businesses, this is a daily process and if this is the case then there is no month end process.

If not the Cashbook enquiry report should be used to produce a reconciliation agreeing the Bank Statement Value, Un-presented Payments and Receipts to the Current System Balance.

Because of the design of the system, it should be unnecessary to reconcile the Cashbook report to the Nominal.

Despite the fact that there is no month end process the enquiry report showing un-reconciled items should be added to the audit pack.

Parts Valuation

Using the Parts reports taken at the end of the calendar month the Parts stock valuation should be calculated. It is important to break the valuation down by Product Group since values are generally held in the nominal by different codes for each product group.

The calculation for Parts stock is: Parts Valuation + WIP value – GINR report = Nominal Value.

This takes the parts valuation and adds to it the parts issued to the workshop from the work-in-progress report and then subtracts items which have been invoiced but are not currently in stock thereby providing a credit to the parts stock when no corresponding debits exist.

In the event of a difference the downloaded parts valuation can be reconciled to the nominal value.

All documents created or used should be considered for inclusion in the month end audit pack.

Parts Provision to Aged Stock

The usual way to deal with Parts provisioning is to take the Parts Valuation and from the aged values calculate the difference between this period, (by age band) and the last period and then calculate the percentage based on the businesses requirements (typically 1-2 years 25%, 2-3 years 50%, over 3 years 100%. Once the value has been calculated a journal debiting Parts Expense and crediting Parts Provision should be completed.

Once completed the reports and journal daybook should be retained as part of the audit pack.

GRNI

At the end of each period, the outstanding value for GRNI should be confirmed against the nominal value outstanding. In the event of discrepancies the report taken at the end of the month from the Purchase Ledger should be reconciled back to the nominal value using the advice note as the reference.

Again all documentation used should form part of the month end audit pack.

Parts Deposits

Using the movement report taken at month end the balance sheet nominal code value for Parts Deposits should be reconciled. The movement report will provide all entries where deposits have been taken. Where the part was later supplied a corresponding debit entry will clear down the original credit. It should be noted that if the original customer order is cancelled by the Parts Department this also will show on the deposits nominal as a debit entry. To ensure this has not been the case the Retained Deposits nominal code should also be included in the reconciliation.

Parts in Transit

Where the Distribution process is being used any items on the Parts in Transit report will be affecting the Parts Stock reconciliation at both sites since nominal movements do not take place until the items are receipted at the receiving end.

Pre-payments

In some cases, it may be prudent to ensure that pre-payments have taken place when these are driven via automatic journals.

Codes with Zero values

At the end of each month a number of codes should be checked as their expected value should be zero, they are as follows.

INTER code INTVM code Dump account (ZZZZZZ) Contra Code.

If any of the above have values these should be traced and corrected either by journal or contra journal.

Also to be considered should be the Miscellaneous Prep Cost Control (or Vehicle GRNI). Dependent on the set up of the vehicle miscellaneous costs process this may need to be reconciled back to the purchase ordering GRNI. If GRNI posting has not been set up then the Control should be reconciled to vehicles in stock over month end with un-cleared postings against them.

Once the nominal has been completed and the profit/ loss has been journaled to the balance sheet then the final total at the bottom of the profit and loss should be at zero, this indicates that the month end can now be run

Any changes or journals or contras carried should be recorded in the month end audit pack.

VAT Reporting

Although the VAT process is completed quarterly and a quarterly report is available the VAT nominal value should be reconciled back to the VAT report each month.

By reviewing a full VAT analysis report against the nominal value for each VAT code (Input, Output, Special Scheme) it is possible to reconcile the values. In the event of an error, the individual values should be checked line by line between the nominal code and the VAT report. Any problems should then be rectified.

At the quarter end, it is important to add the value of the outstanding vehicle deposits difference at the correct VAT rate to the VAT control in order that the VAT is correctly stated for deposits held.

Aftersales Processes

Parts

The end of the month provides an ideal opportunity to review the aftersales operations within the business, although nothing is mandatory, these can be seen as best practice recommendations.

Process all outstanding parts issues

Ensuring all outstanding parts are issued to the workshop and the front counter keeps the stock holdings correct and also aids in accurate parts valuation for reconciliation purposes.

Parts movements report for credits and adjustments

Checking the movement reports for credits and adjustments will provide details of any credits done in the month and any adjustments which have taken place.

Outstanding orders

Check outstanding customer orders for overdue workshop bookings where parts have been reserved, this can also apply for the front counter.

Supplier orders

This report is used to check for outstanding receipts, reviewing any backorders and actioning as necessary.

Perpetual Stock Take Within Pinewood DMS

A perpetual stock take can be done either via bin location or a part number range, this contributes to keeping the stock file accurate.

Negative Stock

This report identifies any parts that currently have a negative stock holding.

End of Day / End of Month

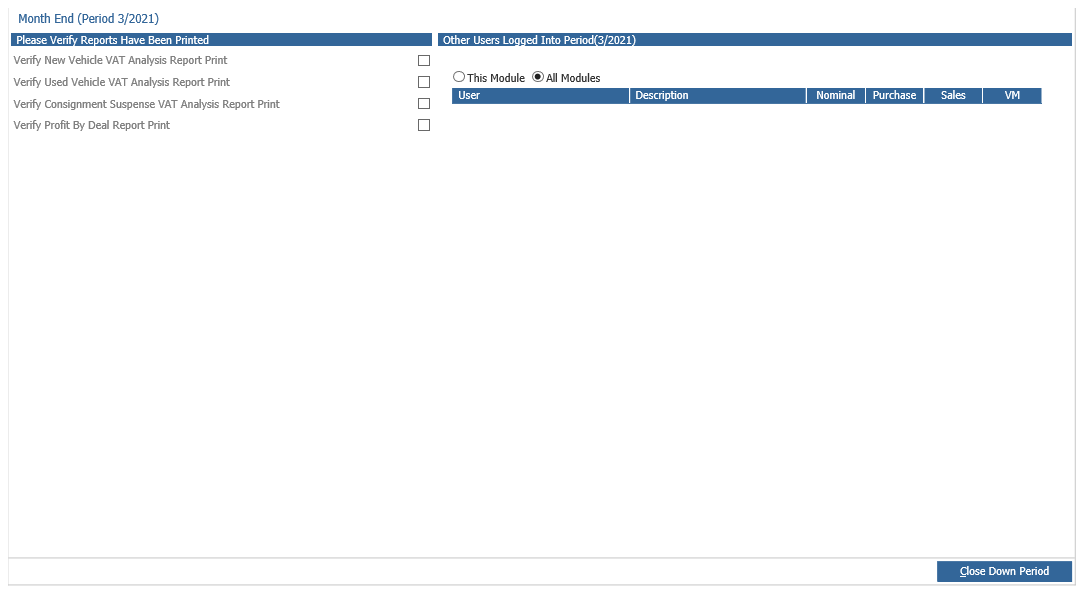

During the EOD many of the reports are also available in a monthly format as indicated by the buttons at the bottom of the screen, if any reports are required for monthly reporting purposes they MUST be printed off before accepting the month end as they cannot be reproduced.

Workshop

Invoice jobs from WIP

Ensure all jobs that can be processed from the work in progress are invoiced off. This can include any outstanding warranty claims if applicable.

Invoice all Internal Jobs

If any internal jobs remain on the work in progress the month end for vehicles cannot be run.

Credits

A report can be generated from within the repair order register to view any credits that have been done throughout the month which can also be downloaded to Excel.

Technicians

Update the technician's holidays within the parameters to ensure the diary accurately reflects the time available for the next month.

End of Day / End of Month During the EOD

some reports are also available in a monthly format, if any reports are required for monthly reporting purposes they MUST be printed off before accepting the month end as cannot be reproduced.

Nominal Ledger Month End

Once the Sales Ledger, Purchase Ledger and Vehicle Ledger have been month ended and all nominal postings and reports have been completed, the nominal ledger can be month ended.

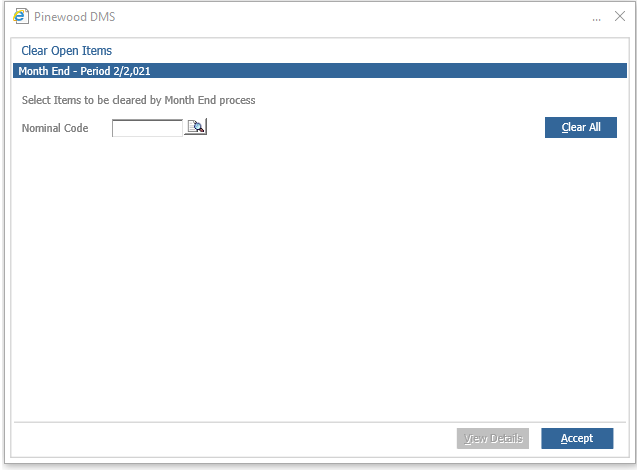

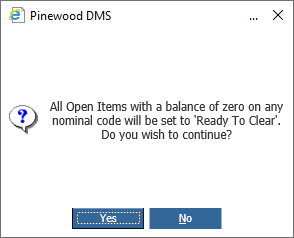

When the Nominal Month End option is selected from the menu, the first thing to be done is to clear down any zero balance against open item nominals.

Previously you would have had to manually select each Open Item nominal code and manually confirm each transaction that had reached a zero balance and that you would want to clear. There is now a Clear All button to the Clear Open Item screen.

This change allows you, should you choose, to set the status on any zero balance item in the period you are closing to Ready To Clear on any nominal code. Having selected this option you are presented with the below confirmation screen.

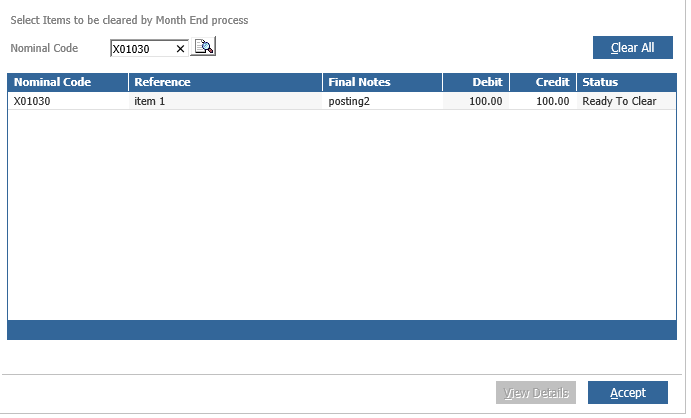

This process ensures that there is no activity on that open item in a future period. If there is, the Open Item will not be presented to be set to Ready To Clear or be included in this process. The previous functionality to allow individual items to be selected and set has been retained. If a single nominal code has been selected you will also have a Clear All button available.

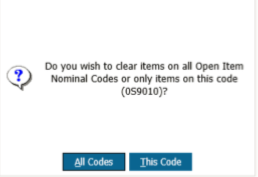

When processing a single code in this way then you will be presented with the option to process all codes or the single code as per the below message.

This allows you to set all items on specific codes to clear if you wish to process Open Items in that way. The archiving of Open Items continues as part of the nominal month end process.

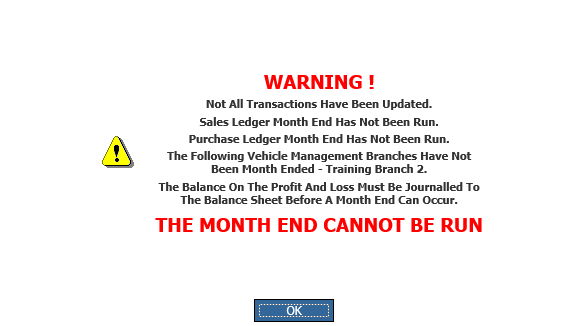

If the nominal ledger cannot be closed, a warning pop up appears giving the reasons.

- These items must be addressed before the nominal can be month ended.

- The sales Ledger must be closed.

- Purchase Ledger must be closed.

- Vehicle Ledgers must be closed.

- The Dump Account ZZZZZZ balance must be zero.

- INTER nominal code balance must be zero.

- INTVM nominal code balance must be zero.

- All transactions must have been updated, use the Update option on the nominal ledger menu to do this.

- The profit/loss for the month must have been journaled to the balance sheet using the ‘Transfer to Balance Sheet’ and ‘Retained Profit’ nominal codes. Please click here for an article on how this is completed.

Once this has all been addressed the month-end process can be attempted again. If successful the following screen will appear.

Click ‘Process’ and enter the month end date for the period that you are closing but for the following year.

This is how the system periods are maintained. This will complete the month end process.